Happy New Year! We’re kicking off our first article of 2024 with welcomed good news:

The Federal Housing Administration (FHA) increased the maximum claim amount on the Home Equity Conversion Mortgage (HECM), the only type of reverse mortgage loan it insures, from $1,089,300 (2023) to $1,149,825 (2024). Not sure what all that means? We’ll explain down below.

In this article, we’ll cover:

HECM Loan Basics

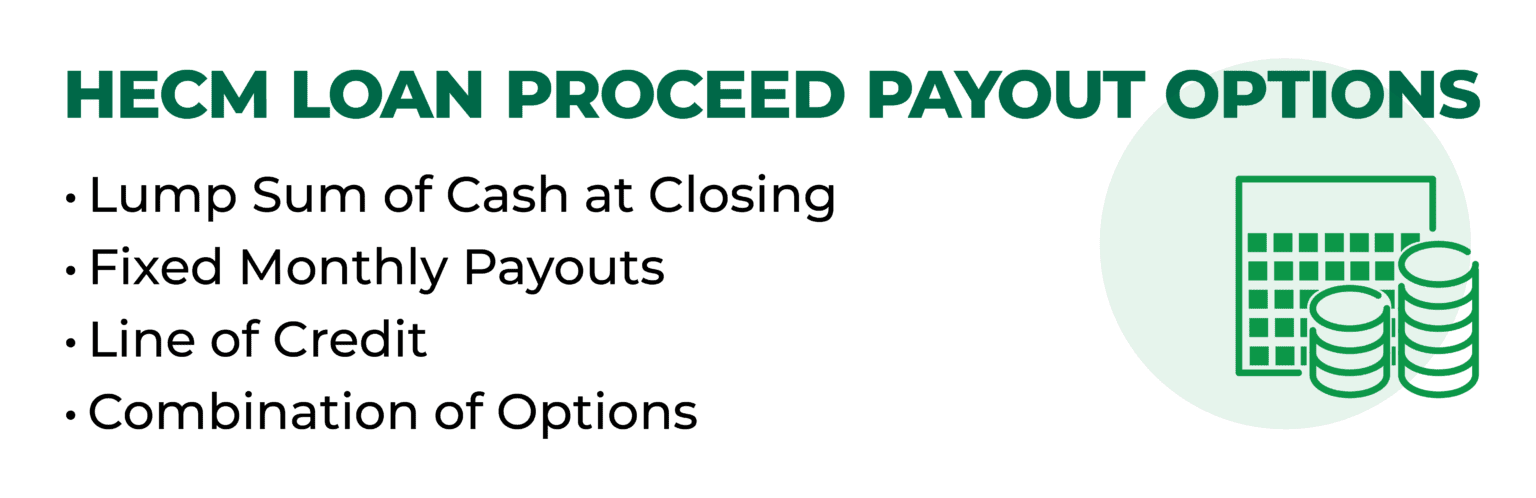

A Home Equity Conversion Mortgage (HECM) is a federally insured loan allowing homeowners 62 and over to convert a percentage of their home equity into a lump sum of cash at closing, fixed monthly payouts, a line credit to use as needed or a combination of these options.

One of the most attractive features of a HECM is the flexible repayment feature. Borrowers can defer repayment of the loan balance to a much later date — typically until they pass away or permanently move out of the home. While HECM borrowers must continue paying critical property charges, like taxes and insurance, they’re not required to make monthly principal and interest mortgage payments.

To learn more about the basics of a HECM, read our article Home Equity Conversion Mortgage (HECM) Loan: What You Need to Know.

Key Factors Determining HECM Loan Payout

While learning about reverse mortgages, you may encounter the term “principal limits.” Principal limits provide a basis for the amount of money an eligible homeowner can borrow. The higher the principal limit, the more money the homeowner can borrow. With the principal limit amount, the lender pays off any existing mortgages or liens affecting the title. The remaining amount, known as the net principal limit, is what the borrower can use for any purpose, such as funding long-term care or establishing a rainy-day fund.

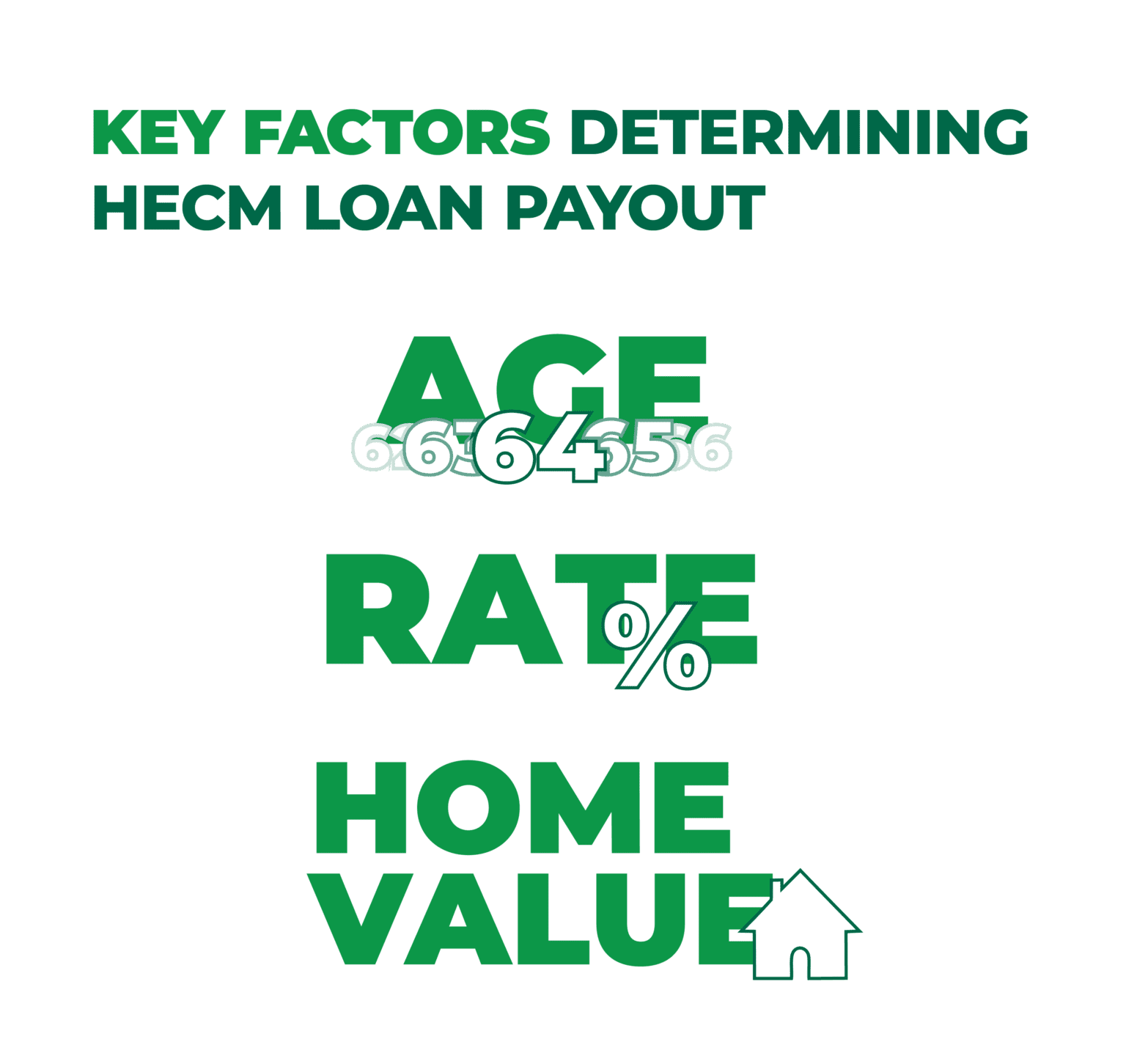

To determine the initial principal limit on the HECM loan, the lender needs to know three key factors:

Age: The age of the youngest borrower or eligible non-borrower spouse factors into the calculation because younger borrowers, or borrowers with a younger eligible non-borrowing spouse, will generally qualify for less HECM loan proceeds.

Rates: The long-term interest rate, or the expected rate, on a HECM loan also factors into the principal limit calculation. For adjustable-rate HECMs, lenders typically arrive at the expected rate by adding the weekly average of the 10-year Constant Maturity Treasury (CMT) index to a margin that the lender sets. Higher expected rates produce lower principal limits, while lower expected rates produce higher principal limits.

Home Value: Lenders use the lesser of the appraised home value or the 2024 HECM limit of $1,149,825. The lesser value is called the maximum claim amount (or the HECM limit).

Generally speaking, the younger the borrower, the higher the home value, the lower the expected rate — the greater the principal limit.

Why the HECM Limit Increase Is a Good Thing

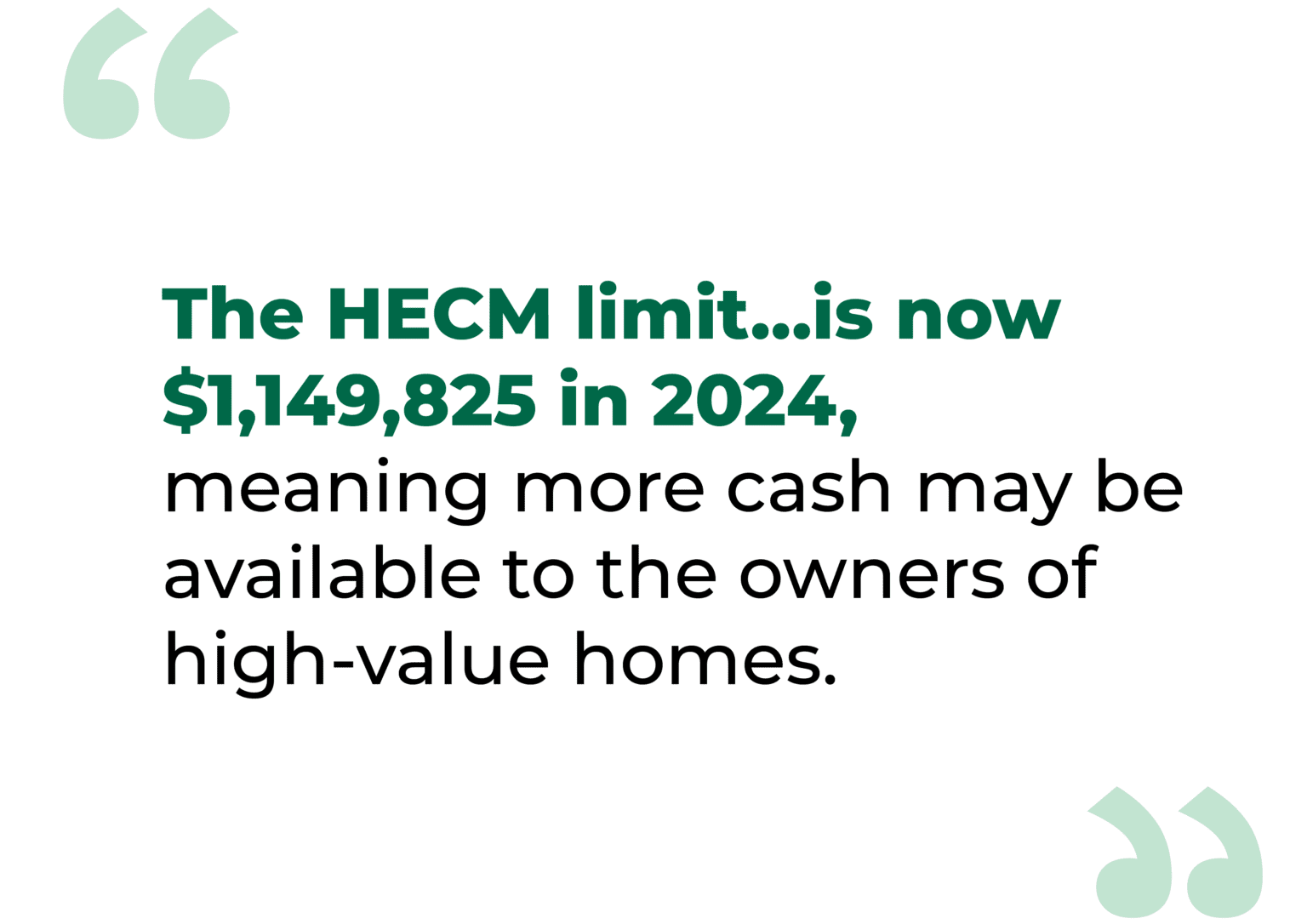

With the HECM limit enhancement, borrowers with higher home values (e.g., a home worth $1.4 million) can access additional equity compared to previous years. Remember, when calculating the principal limit, lenders use the lesser of the appraised home value or the current HECM limit. The HECM limit was $1,089,300 in 2023 but is now $1,149,825 in 2024, meaning more cash may be available to the owners of high-value homes.

Here’s a hypothetical comparison of a 69-year-old borrower using the principal limit factor table supplied by the FHA and utilized by all HECM lenders. For this calculation, the home value is $1.5 million, and the expected rate is 7.0%.

- 2023 Available Loan Proceeds (Principal Limit): $397,594

- 2024 Available Loan Proceeds (Principal Limit): $419,686

That’s an increase of $22,092.

NOTE: Story is for illustration purposes only. The persons depicted herein are fictional and any resemblance to actual persons is a coincidence.

A higher principal limit can benefit those taking out a new HECM and those refinancing an existing HECM. In some cases, achieving even a slightly higher principal limit can mean the difference between being short to close (the borrower would have to bring funds to closing to cover an equity shortfall) versus not (the borrower wouldn’t have to bring funds to closing).

It’s Advantageous to Lock in the Expected Rate

After applying for a HECM, consider locking in the expected rate, as the rate could swing higher or lower between application and closing based on market conditions. A higher rate at closing could reduce the amount of loan proceeds you’d be entitled to.

To put it briefly, the expected rate lock protects the principal limit against a potential rise in the expected rate and is good for 120 days from the date the FHA case number is assigned. If the expected rate falls after you lock, you should benefit from using the lower expected rate at closing.

Let’s Start a Conversation!

Are you considering a reverse mortgage loan and wondering if now is the right time to put your home equity to work for you? At Fairway, we’re here to help you learn about HECM loans so you can make an informed decision about one of your most valuable retirement assets: your home equity. Connect with us today!

Copyright©2023 Fairway Independent Mortgage Corporation (“Fairway”) NMLS#2289. 4750 S. Biltmore Lane, Madison, WI 53718, 1-866-912-4800. All rights reserved. Fairway is not affiliated with any government agencies. These materials are not from HUD or FHA and were not approved by HUD or a government agency. Reverse mortgage borrowers are required to obtain an eligibility certificate by receiving counseling sessions with a HUD-approved agency. The youngest borrower must be at least 62 years old. Monthly reverse mortgage advances may affect eligibility for some other programs. This is not an offer to enter into an agreement. Not all customers will qualify. Information, rates and programs are subject to change without notice. All products are subject to credit and property approval. Other restrictions and limitations may apply. Equal Housing Opportunity.